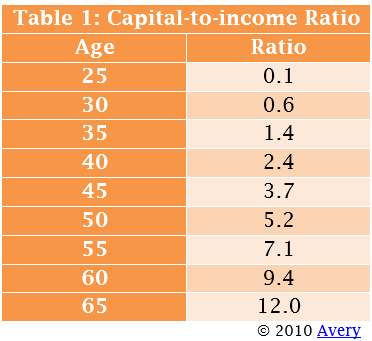

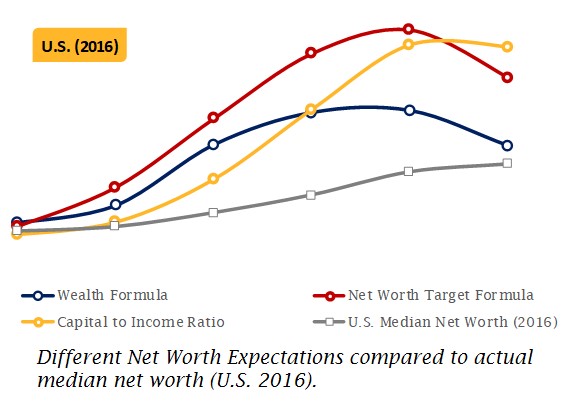

Using the median gross incomes together with the median age (25 ≤ 34 gives 29.5; ending at age 79.5) of the population given in the table above we can begin to make a comparison of the four formulae in the graph below (U.S. shown, Dutch gives exactly the same trend). First thing to note is that the Wealth – and Target formulae don’t handle the decrease of income in retirement (after 65) very well, also the Capital to Income Ratio is built to work until age 65, so it is not surprising that it too breaks its trend after this age.

Overall, I think that the Capital to Income Ratio works best – with a nice S-curve allowing people at a young age to build up slowly. In contrast to both the Wealth – and Target formula which see an almost linear increase from the start albeit one steeper as the other (difference in savings rate). Using the Money Guy modification (used in graph), the Wealth formula is improved to also show more of an S-curve for the early years.