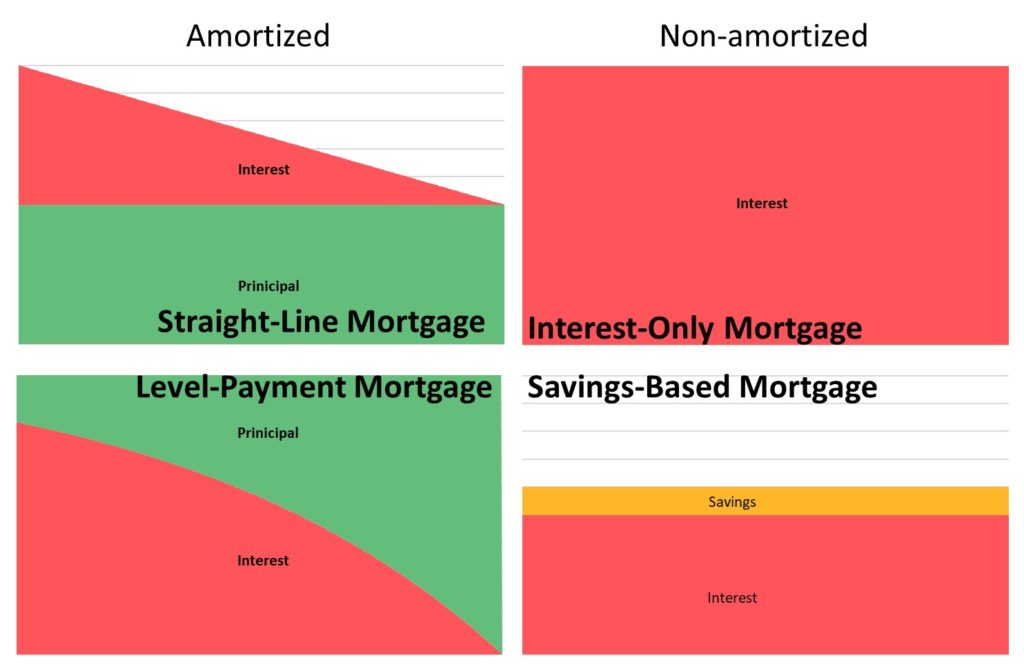

Let’s introduce the types of mortgage one can find in the Netherlands for a house to live in (excluding rental properties). I will try to use American terms to describe them, but be aware that they might not be synonymous to the American equivalent. Let’s begin with the currently main two types of amortized mortgages, the level payment mortgage (‘annuïteitenhypotheek’ in Dutch) and the straight-line mortgage (‘lineaire hypotheek’ in Dutch). Both will be paid off in full after the original term has passed – since 2013 a maximum of 30 years.

The main difference being that with the level payment mortgage, as the name suggests, the monthly payment stays equal – starting out with a lower payment of principal and a monthly decreasing interest payment (leading to an increasing payment of principal to keep the monthly payment equal).

With the straight-line mortgage, the principal payment stays equal, with a decreasing monthly interest payment, leading to a decreasing monthly payment.

In comparison, the level payment mortgage is usually more interesting for first time buyers, as the monthly payments start at a lower amount – however the overall interest paid over the mortgage during the total life time of the loan is less for the straight-line mortgage. The second option would therefore be a more viable option, economically, if you can afford it. Usually people tend to earn more money only later in life and the first option would probably be more viable, practically, at an earlier age.