It used to be in the Netherlands that your student scholarship was turned into a ‘gift’, that no longer needed repayment, if you would get a degree within 10 years. This system build was significantly however altered in 2015 with the replacement of a grant and loan system with only a student loan system. Basically, going more towards an American system just as Dutch health care had done a few years earlier, perhaps I’ll talk about the Americanization of the Netherlands (financially speaking) more in a future post.

This, of course, led to more students needing a student loan in order to be able to afford to get a bachelor’s and/or master’s degree. As a ‘compensation’, student loans that were forced onto students from 2015 onwards were counted in a lighter degree on a credit score compared to students who took a ‘voluntary’ (although often still heavily needed, but definitely not always) student loan in the prior years.

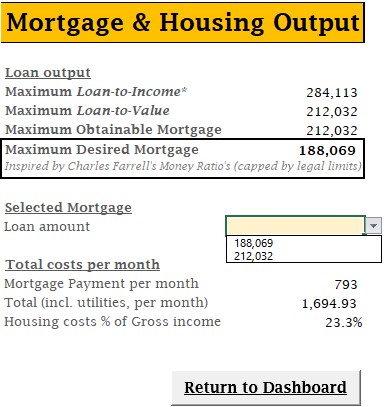

Student loans affect the monthly amount that can be spent on the mortgage – with the old system (prior 2015) requiring 0.75% of the original amount (independent of the current outstanding balance) to be deducted. As an example, a 10,000 debt would in this case reduce the monthly availability by 75.

In the new system (2015 and onwards) the same goes, but with only 0.45% to be deducted. In the same example leading to a reduction by 45.

This doesn’t seem like much – but on a 30-year mortgage, with an interest rate of 1% this means that with a 10,000 debt obtained prior 2015, your maximum mortgage is reduced by 23,318, while in the new system there would be a reduction of ‘only’ 13,991 – a difference of almost 10,000!