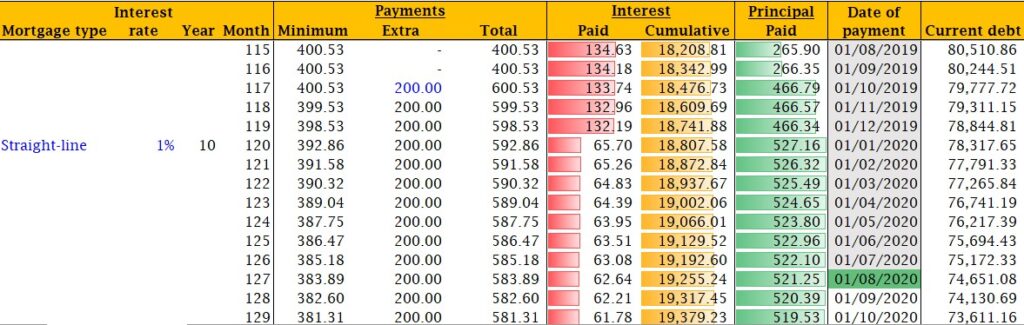

The following section is about the monthly payments, the minimum payments, which cannot be altered as they are based on the input given previously. Any extra payments you wish to do, in this example 200 was added, this is repeated until you put it back to 0 (or another amount). The total monthly payment, which is the addition of the minimum – and the extra payment.

After that, two columns about the interest payments, the interest paid for that month (with a red bar showing how this is changing over time), and the cumulative interest paid (with a golden, increasing, bar showing the progress). The next column accompanies the interest paid per month and this is the principal paid per month (the amount that is reducing your loan).

The next column tells you about the date this payment occurs, with greyed out dates being in the past, the green date being the current month and the white months still in the future. The last column tells you the status of the total debt remaining in that particular month, assuming that the previous columns have been filled out properly. This column can be altered, as the extra payments, when done on another date then the date of payment, can change some details (pennies) in the principal/interest payment balance. By altering the current debt, you can bring the amortization schedule back in line (but the impact is minimal).

Side note: inside the worksheet is the option to collapse this amortization schedule on a yearly basis. This has however been blocked in order to prevent mistakes to happen with the less experienced user – this might alter in the future, and therefore has not been removed. Reach out to me if you’re interested.