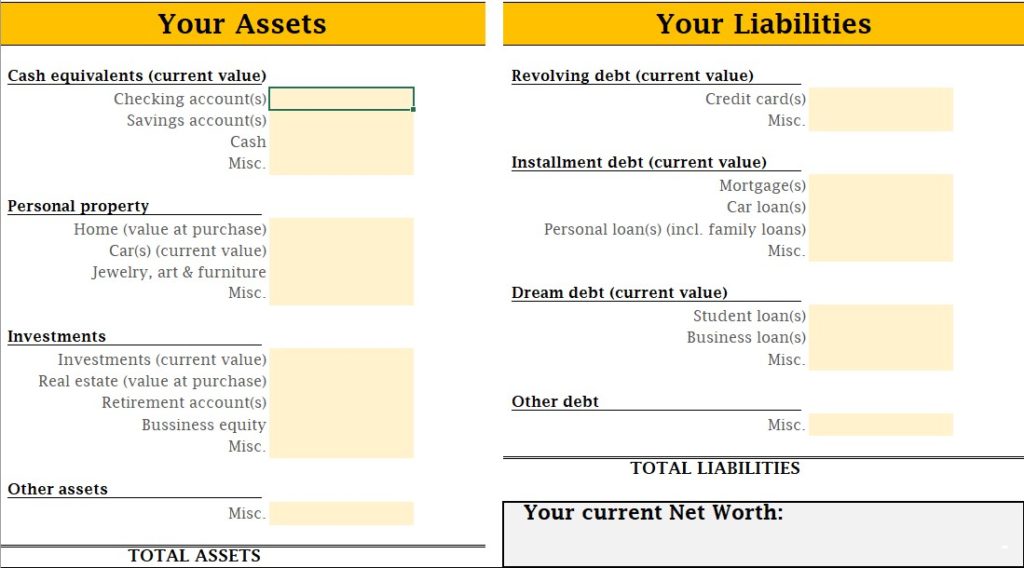

Now we are getting into a more complicated category. This category includes your home, and I’ll begin with something that people might not agree with – don’t use the current estimated value of your house.

With the world-wide web supporting you, it is getting easier and easier to find your house’s current market value using websites like Zillow.com (U.S.) or huispedia.nl (NL). Alternatively, in the Netherlands as probably also in the U.S., the municipality gives a value to the home annually for the purposes of taxes (the Dutch Valuation of Immovable Property Act or VIP act, ‘WOZ-waarde’ in Dutch), also discussed in my article on mortgage taxes (check historical house values for the VIP act here (Dutch)). Government appraisals are usually not comparable to a market value though!

Appreciation on paper is just that – meaningless unless you are actually going to sell your home right now. The main hurdle is to remove the persistent notion that a home is an investment, it is not! In fact, this is one of the main messages of Robert Kiyosaki’s Rich Dad, Poor Dad. A home is a used asset, you are living there, building memories – not selling it for a quick profit (usually). Therefore, I am a fan of using the value of the house at the cost that you’ve bought it for – limiting the feeling of net worth growth, just because my home is growing in value.

The inverse is true for the next part of this category, the car(s). A car is barely an asset as it depreciates very quickly, with most of its value lost in the first 3 years after leaving the factory. Therefore, do use a current estimate for the market value of your car, instead of the original price you’ve paid for it – it isn’t worth anywhere near that anymore! Also for this there are resources available such as the blue book (U.S.) or the ANWB (NL).

The last part of personal properties involves any valuable of reasonably high values, this includes things such as art, jewellery or perhaps furniture. Personally, I feel this is not really a part of your net worth. However, but if you would be following the book “Your Money or Your Life” by Vicki Robin and Joe Dominguez, one of the biggest inspiration of the FI/RE movement, you would be going around your house determining the current market value of every trinket in your home! As long as you stay consistent, any approach is valid for you.

It’s very useful information. Thanks for sharing! one question related with investment though (bonds for example), why current value is used for calculation? isn’t similar like a house current value – meaningless unless i sell it?

Happy to hear you liked it! You are absolutely right that a current value of an asset is meaningless unless you sell it right now. Two financial philosophies on that:

From a philosophical perspective, money in the bank is ~technically~ also meaningless unless you spend (or invest) it.

From a financial perspective, unlike a home, stocks and bonds can be sold at any given point (during business hours) and therefore could be close to cash. Next to this, can also invest in currency on the stock market – therefore kind of investing in cash.

Money in your bank account also rises and falls with each bill or paycheck that comes in, just like your stock portfolio will rise and fall from day to day. In the end, it is up to you what you want to take into account for your net worth.