There are a few conditions that need to be met (in the Netherlands) in order to be eligible for this deduction of your interest though, including:

- The mortgage is (fully) used to buy, improve or maintain your home (not a commercial property – and not using a part of the loan for something like a car).

- The home is your main place of residence (not a holiday – or second home).

- You will repay the mortgage within 30 years and is a level-payment – or straight-line mortgage (for mortgages started in 2013 or after).

- After selling a home, when you have surplus value and you buy a new home within three years, you can only use the deduction if the surplus is used for the new home.

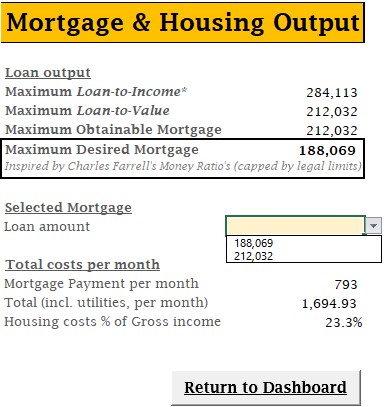

If you have yet to get a Dutch mortgage – and you want tax benefits – you are stuck to choose an amortized mortgage, either the straight-line or the level-payment mortgage. Although with the decreasing mortgage rates, there is a new influx of people choosing for a non-amortized mortgage type, as the tax benefit no longer outweighs the decreased monthly costs. I am no financial advisor, but for those on the path to (early) financial freedom it should be mathematically clear that never getting rid of your mortgage will not get you there, as the debt will never be cleared until the end of your term – if you’re not unlucky.

If you already had a mortgage before 2013, the deduction can still only be applied to a maximum of 30 years, with mortgages starting before January 1st 2010 having a deadline of 31st of December 2039. After these 30 years you can no longer deduct any interest, increasing the effective costs of your mortgage.